Each quarter, Fusion Worldwide's analysts dive into the earnings calls of leading electronics manufacturers to uncover the latest demand trends in the electronic component market. By examining these reports, they identify key developments that shape the industry, from shifts in technology to evolving market dynamics. The following insights reflect the most significant trends impacting demand across various sectors.

AI and ML Propel Growth Across Several Sectors

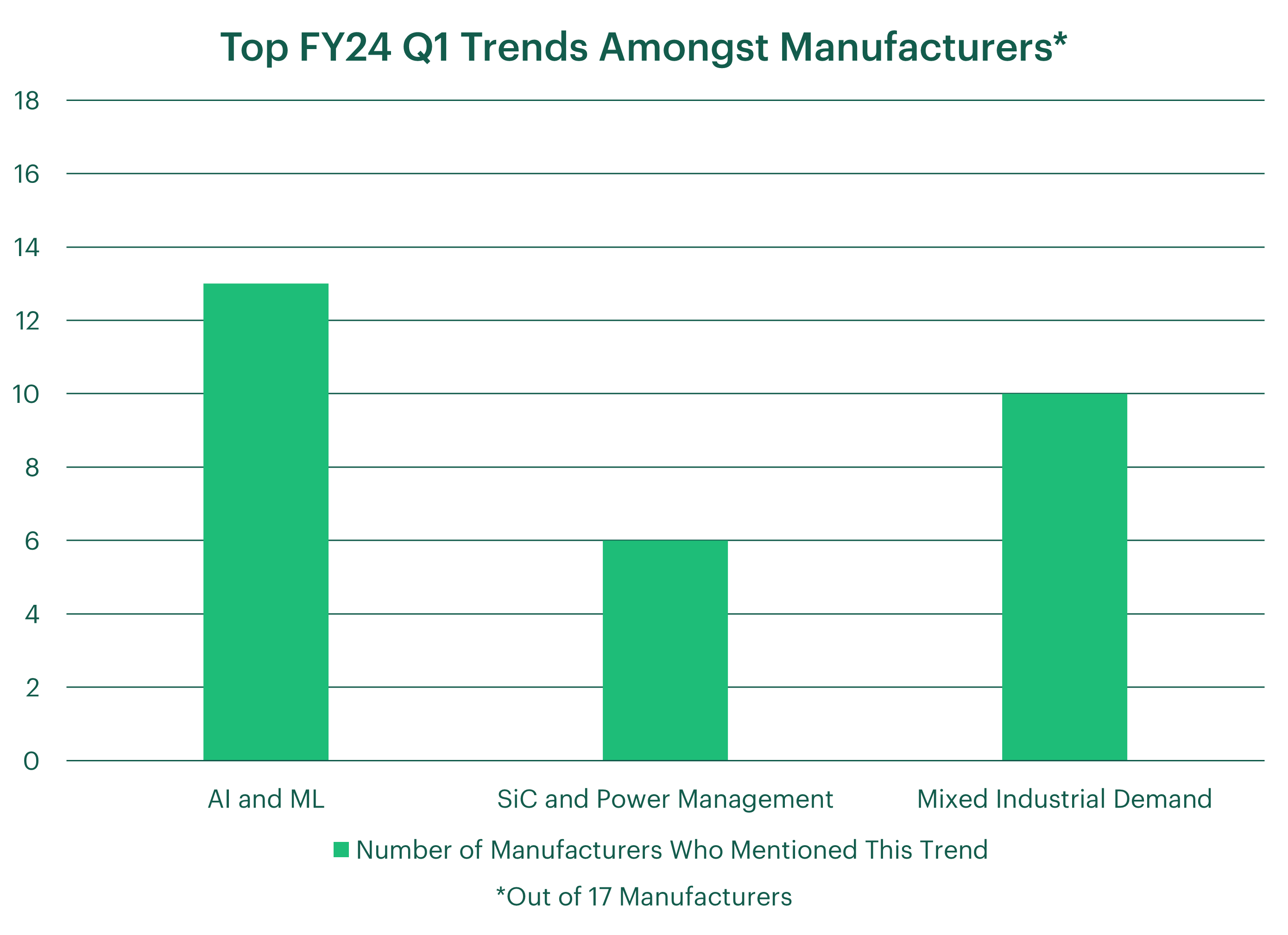

Of 17 manufacturers, 13 mentioned artificial intelligence (AI) and machine learning (ML) as key business drivers.

Advanced Micro Devices (AMD) saw AI and ML drive growth for the data center business, as evidenced by the number of MI300x deployments at major tech firms for generative AI training. This growth extends to the client segment, with an 85% YOY increase in revenue fueled by Ryzen mobile and desktop processor demand. AMD consequently increased its data center GPU revenue outlook from $3.5B to over $4B, underscoring the pervasive impact of AI and ML across industries.

Intel Corporation saw AI and ML lead demand trends, and the company anticipates strong AI-related growth opportunities. AI PC CPUs are projected to ship 40 million units in 2024. The Gaudi Accelerator Series is gaining momentum, with over 20 customers adopting Gaudi 2 and 3. The launch of the Open Platform for Enterprise AI Project aims to accelerate GenAI deployments.

MaxLinear Inc. anticipates AI adoption for cloud applications and is poised to fuel the transition to higher bandwidth data infrastructure. Additionally, early-stage revenues from AI-related design wins contribute to growth, with expectations for greater production later in the year. These trends will likely contribute to revenue expansion in storage-related products, Ethernet connectivity, and broadband markets.

ON Semiconductor Co. (onsemi) saw healthcare and data center revenue increase thanks to AI applications, reflecting industry momentum. Onsemi anticipates a 22% Compound Annual Growth Rate (CAGR) in the cloud and data center market over the next five years, so the company is aligning business to expand alongside demand.

Notably, Onsemi's AI technology is integrated into half of the over-the-counter hearing aids, further illustrating its impactful presence across diverse sectors.

Qualcomm Incorporated's AI-powered Snapdragon platforms are gaining traction in premium-tier smartphones. The Snapdragon Digital Chassis drove 35% YOY growth in automotive revenue, supported by automotive AI. AI diversification across industrial, automotive, and networking segments is fueling Qualcomm's profits.

Renesas Electronics Co’s AI-related demand was minimal, contributing single-digit percentages to total sales, but it still presented an interesting development. This trend increased DDR5 adoption, leading to growth in the company’s data center and infrastructure business, which forecasts show will continue.

Samsung Electronics Co. noted that generative AI is fueling demand for high-value memory products like High-Bandwidth Memory (HBM) and Solid-State Drives (SSDs). The company expects generative AI to continue driving demand for HBM and high-density DRAM. This trend fueled its decision to shift production capacity to high-value products, aligning with rising ASPs across DRAM and NAND segments.

Sanmina Co. strategically leverages AI demand to propel cloud network upgrades and augmented reality traffic, expanding its Optical Advanced and Packaging segment to accommodate AI applications. With investments in optical advanced packaging and server storage tailored for AI, the company is poised to capitalize on the growing opportunities in this sector.

Seagate Technology Holdings noted that AI drove demand for cost-efficient mass storage, which boosted HDD business. The company expects healthy nearline demand growth throughout the year, driven by AI-generated content and server growth.

Silicon Laboratories Inc.’s Series 2 platform, featuring AI/ML capabilities, gained traction in industrial and commercial markets. AI/ML capabilities are becoming crucial in products like the xG26, driving demand.

STMicroelectronics N.V. (STM) is expanding its MEMs sensor portfolio to capture edge AI demand. To align with trends in the AI-related markets, the company is launching a sensorless tire-pressure monitoring system for e-bikes. Additionally, STM’s ongoing partnership with Compuware is helping the company gain traction in high-performance telecom and AI server power supplies.

Taiwan Semiconductor Manufacturing Co. (TSMC) stated that demand from AI-associated data centers represents one of the most robust market opportunities, creating a significant growth area for TSMC, especially within energy-efficient computing. AI is also partially driving HPC-related demand, another trend from which TSMC hopes to profit. TSMC consequently expects AI-related revenue to double in 2024.

Western Digital Co. recorded increased demand for mass capacity storage thanks to AI adoption, which drove strong profitability for WD’s HDDs. AI also contributed to the rising demand for NVMe SSDs.

Electric Vehicle Demand Sparks Investments in Silicon Carbide and Power Management Devices

Six of the 17 manufacturers discussed the demand for silicon carbide and advanced power management technologies due to electric vehicles (EVs) and renewable energy sources.

ON Semiconductor Co. (onsemi) recorded more demand for silicon carbide and IGBT products thanks to the electric vehicle industry, leading to plans to ramp up 200-millimeter silicon carbide substrates in 2025. Additionally, automotive demand continues shifting towards high-resolution image sensors for ADAS systems, providing another boost for the growth of silicon carbide.

Qorvo Inc.’s design wins for secure access in electric vehicles and Wi-Fi 6E solutions bolstered the automotive industry. The power management business is also expanding with design wins in motor controls and power tools.

Renesas Electronics Co. noted that power solutions and silicon carbide technology are driving growth in the automotive sector, with production set to increase in the second quarter. Forecasts indicate that the next four years will likely bring steady growth within the automotive industry.

Sanmina Co.’s main focus was aerospace and defense, but the company also noted EVs as a prominent area of strength.

STMicroelectronics N.V. (STM) is honing its electric and hybrid vehicle technologies, signaling it will focus on these sectors in the coming quarters. Additionally, automotive-focused microcontrollers achieved wins in traction inverters, e-compressor controllers and smart fuses, which showed an uptick in demand for advanced power management technologies.

Wolfspeed Inc. is increasing silicon carbide production to target the EV sector. The company’s investment in Mohawk Valley and Building 10 manufacturing facilities focuses on silicon carbide production for EVs. Approximately 80% of the company's design-ins are for EV applications, showing robust demand for silicon carbide devices.

Industrial Sector Faces Inventory Challenges Amidst Varied Market Conditions

Out of 17 manufacturers, 10 called out mixed trends in the industrial market. Some struggled with excess inventory, while others saw pockets of strength boost their recovery.

Advanced Micro Devices (AMD) recorded a decline in its embedded segment, whose profits fell 46% year over year due to weaker demand in industrial segments and a decrease in communication and automotive business.

NXP Semiconductor N.V. was amongst those that saw improvements in its industrial market, with growth in China partially offsetting softness in Europe and the Americas.

ON Semiconductor Co. (onsemi) struggled with persistent inventory digestion across the industrial market, but there was some stabilization towards the end of Q1. Despite the industrial industry's challenges this quarter, forecasts for industrial business appear optimistic, indicating growth will return towards year-end.

Renesas Electronics Co. and Texas Instruments Inc. (TI) noted that their industrial segments experienced a slowdown in demand. Wolfspeed Inc.’s industrial market also experienced some challenges due to inventory buildup, particularly among Asia-based customers.

Both Renesas and TI noted that forecasts are optimistic as customers continue to work through their excess supply through the end of the year. However, this varies depending on the customer and market segment.

MaxLinear Inc. and Silicon Laboratories Inc. saw industrial revenue expand this quarter, partially attributed to AI-related trends.

STMicroelectronics’ N.V. (STM) industrial segment struggled with inventory digestion as it is taking longer than expected to correct excess supply. The sharp decline in general-purpose microcontroller demand, which predominantly serves the industrial market, is also projected to continue. Due to these forecasts, STM anticipates substantial pricing pressure on the microcontroller and broader industrial sectors.

For More Information Straight From the Source’s Mouth

Dive deeper into the trends discussed above by reading the comprehensive analysis of each manufacturer’s quarterly report in From the Source's Mouth.

How can Fusion Worldwide support your supply chain? Contact us today to speak directly with a representative.